Lower Middle Market Private Equity

You might have noticed that there are a variety of distinctions within private equity: small business, lower middle market, middle market, and upper middle market. Pinpointing the differences among them can be confusing and seem irrelevant to everyday business tasks. But there may come a time when this knowledge matters; if you are considering selling your business to private equity, knowing which firms would be interested in your company is the first step.

In this post we break down the difference between lower middle market private equity and small business private equity— or really small business investing— and how firms may vary from one tier to the next.

What is Lower Middle Market Private Equity?

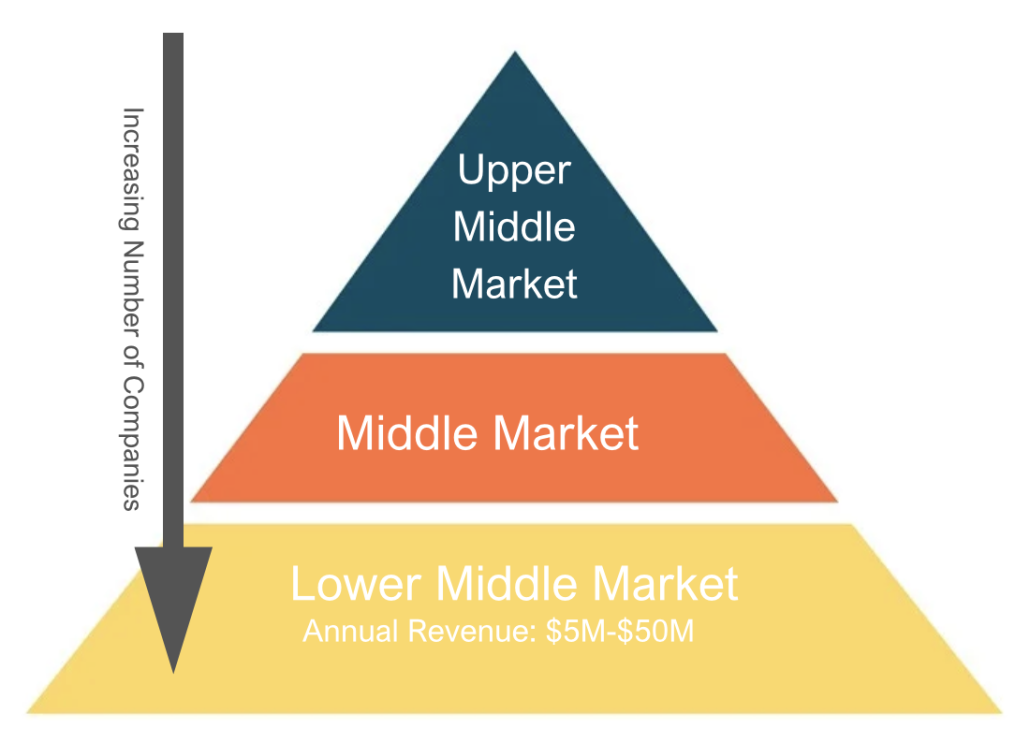

As the phrase suggests, lower middle market private equity is private equity that serves the lower middle market. Most businesses fit within the lower middle market, though the exact definitions vary. One metric considers lower middle market revenue to range from $1 million to $40 million annually, while another defines it as $5 to $50 million.

Why Do Private Equity Firms Like the Lower Middle Market?

The large number of companies in the lower middle market space is one reason why private equity firms often focus on it. In short, more companies equals more investment opportunities. But there are other reasons too. Companies in this sector frequently trade at lower purchase multiples than companies in the middle or upper middle market.

What are purchase multiples? We talk more about purchase multiples, also called EBITDA multiples, here. In short, purchase multiples are factors multiplied with a company’s EBITDA to arrive at the enterprise value, or what the company could be sold for. While purchase multiples vary depending on the company and industry, generally companies in the lower middle market sell at a lower purchase multiple than larger businesses. Put plainly, this means private equity firms make a smaller initial investment when purchasing a lower middle market company.

After the private equity firm’s period of ownership ends, the firm has had the opportunity to grow the company’s value in two ways. Say, for example, the firm grew the company’s EBITDA from 10 to 20 million. This alone is a large value increase— but it comes with a bonus. Companies in the middle market usually sell with a higher purchase multiple than companies in the lower middle market. So, this company would be worth more than double it was in the beginning, through gaining a higher purchase multiple. In finance terms, this concept is called multiple arbitrage. For clear reasons, this is also appealing to private equity investors.

Opportunities for Business Improvement

In addition to the multiple arbitrage that comes with bringing a company up to the middle market, companies in the lower middle market offer another opportunity. Many companies in this space have grown impressively on their own, but have not yet gained from an institutional investor. Meaning, maybe the company could benefit hugely from the latest technology, a new software package, or upgraded machinery. But, without significant capital, the company cannot make such purchases, and thus cannot jump quickly into the next phase of growth.

If an institutional investor— an investor with those financial resources— were to acquire the company, the investor could immediately purchase needed upgrades. This alone can kickstart company growth. This is appealing to private equity firms because it can be a simple, and often relatively fast, way to take the company to the next level. And when most private equity funds’ business ownership wraps up within 5 years, growing a company as much as possible within that time frame is often the goal.

Unlike most firms, 1719 Partners operates without a predetermined investment end date. This means 1719 can take its time to make operational improvements, making sure the company is ready for a change before introducing it.

Small Business Private Equity

Small businesses, as the name implies, report smaller revenue than lower middle market companies. Just as the exact revenue values vary for the lower middle market, the numbers also vary for small businesses. As a small business private investment firm, 1719 Partners generally focuses on acquiring companies with $5 million to $20 million in revenue. An additional metric 1719 looks for is an EBITDA of $1 to $4 million. As you may have noticed, there is an overlap between “small businesses” and “lower middle market businesses.”

The difference matters more in practice. When lower middle market private equity firms will not consider a company because its enterprise value is too low, small business private equity can be the solution.

Small Business Private Equity Firms vs. Lower Middle Market Private Equity Firms

A small business and a company on the higher end of the lower middle market are significantly different sizes. Just as companies in the lower middle market have more employees, private equity firms investing in those companies often have larger management teams. That means it is not uncommon for firm owners to simply advise the president at board meetings, without being directly involved in company changes.

In contrast, due to the firm size, small business private equity firms are often more hands-on and active than their peers at larger private equity firms. The smaller firm members can support the smaller businesses’ management team. For example, the firm’s owner may step in and manage the banking relationship or assist business development in its search for an add-on acquisition.

Neither option is better or worse than the other, rather different private equity firms are better suited to different companies. More robust management teams of larger firms may be better equipped to work with larger, more developed companies, while smaller firms are able to make changes efficiently in a smaller company. 1719 enjoys taking a very hands-on approach to its portfolio companies, stepping in to actively create the changes that would most benefit the company.

Selling to Private Equity

There are many benefits of selling to a private equity firm: financial resources, management expertise, professional connections, and more. But as mentioned above, it is important to sell to the firm that would create the most impact for your company’s size and potential. 1719 Partners’ thoughtful, active approach allows us to make positive changes at a pace that is in the company’s best interest; our indefinite investment timeline means 1719 Partners has the patience to create true long-term value vs. a quick flip. If you have any questions about the types of private equity firms, or are curious about the 1719 difference, please contact us.